May 20, 2024

Securing affordable primary care for all Australians

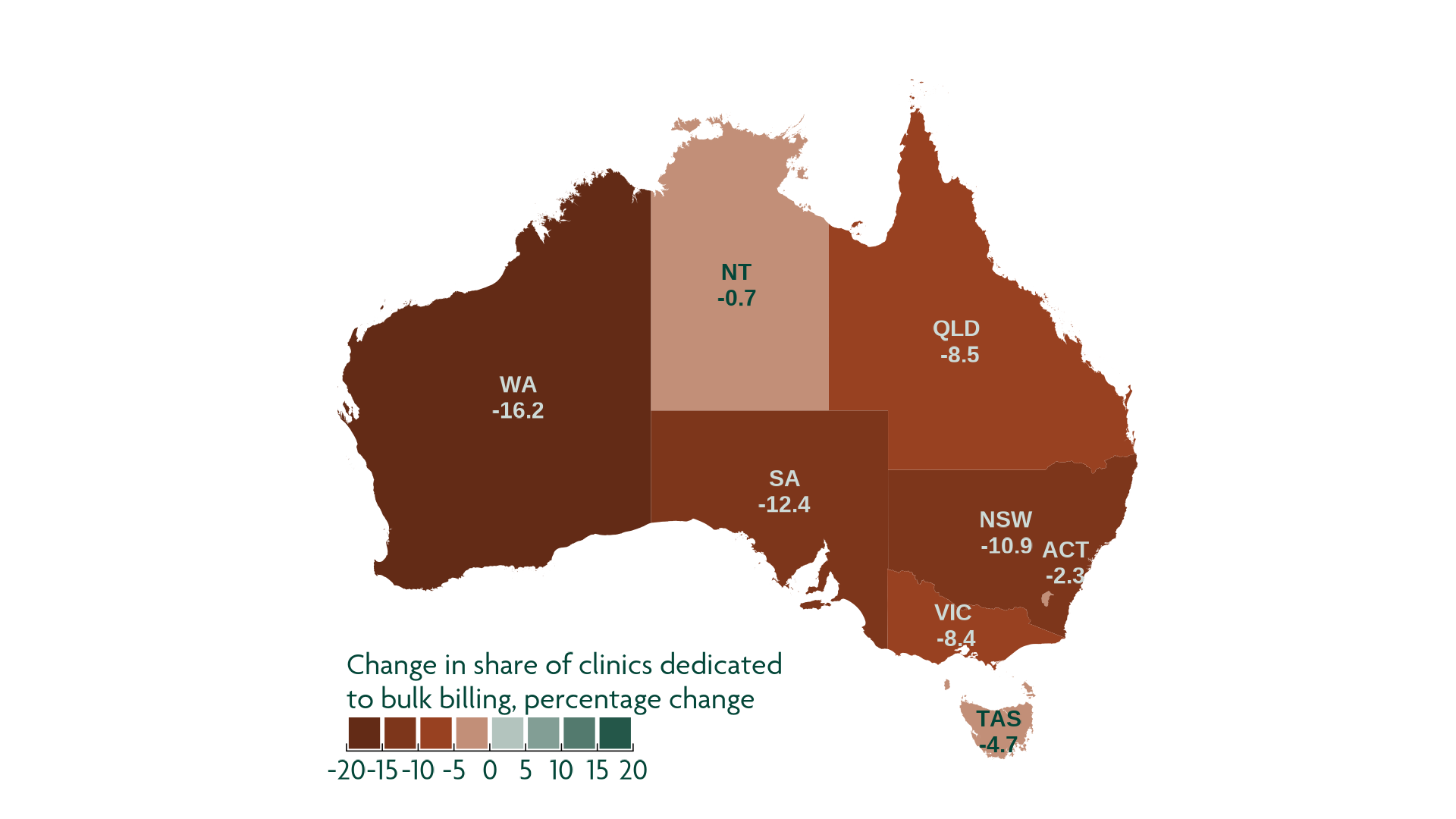

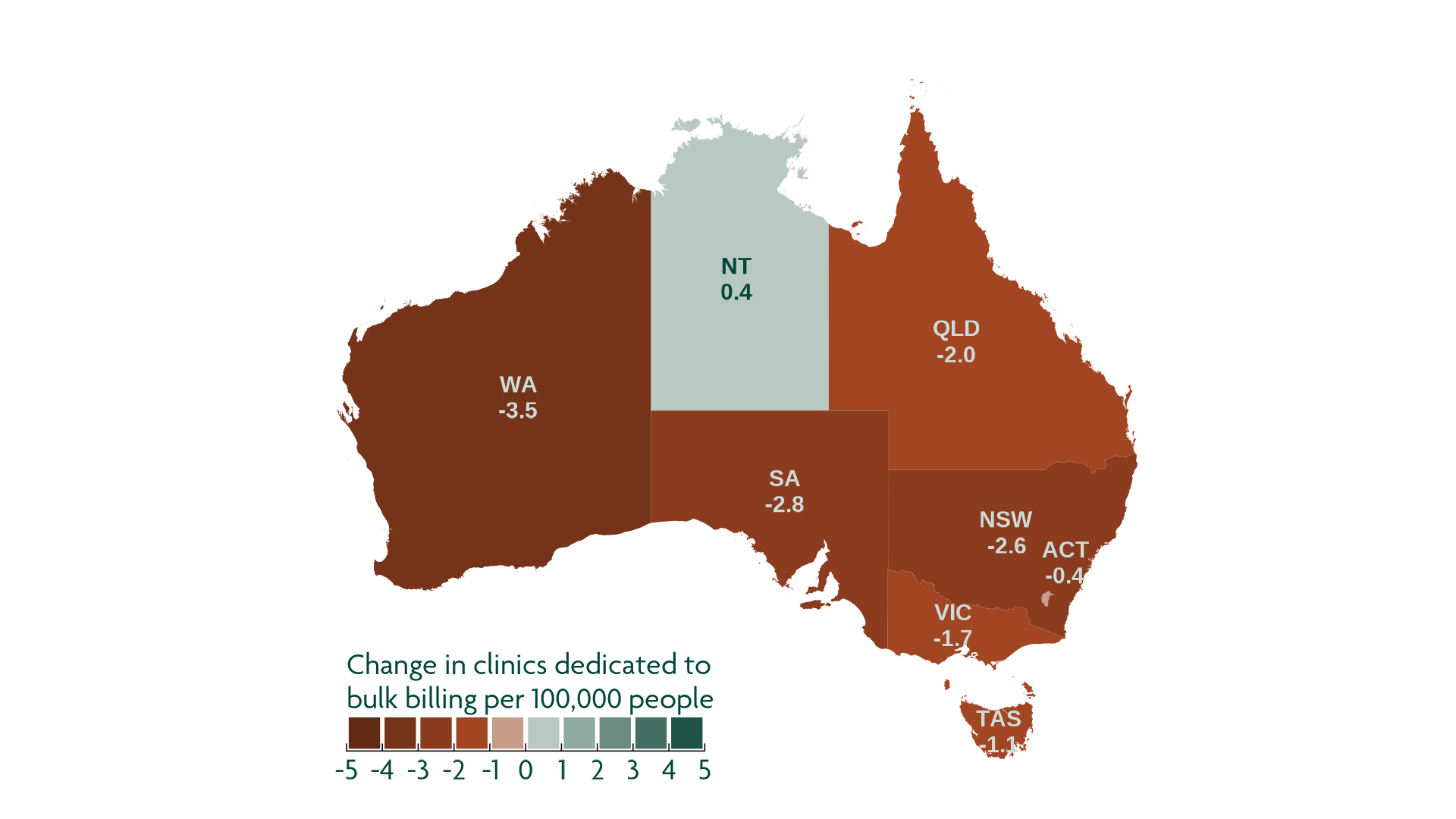

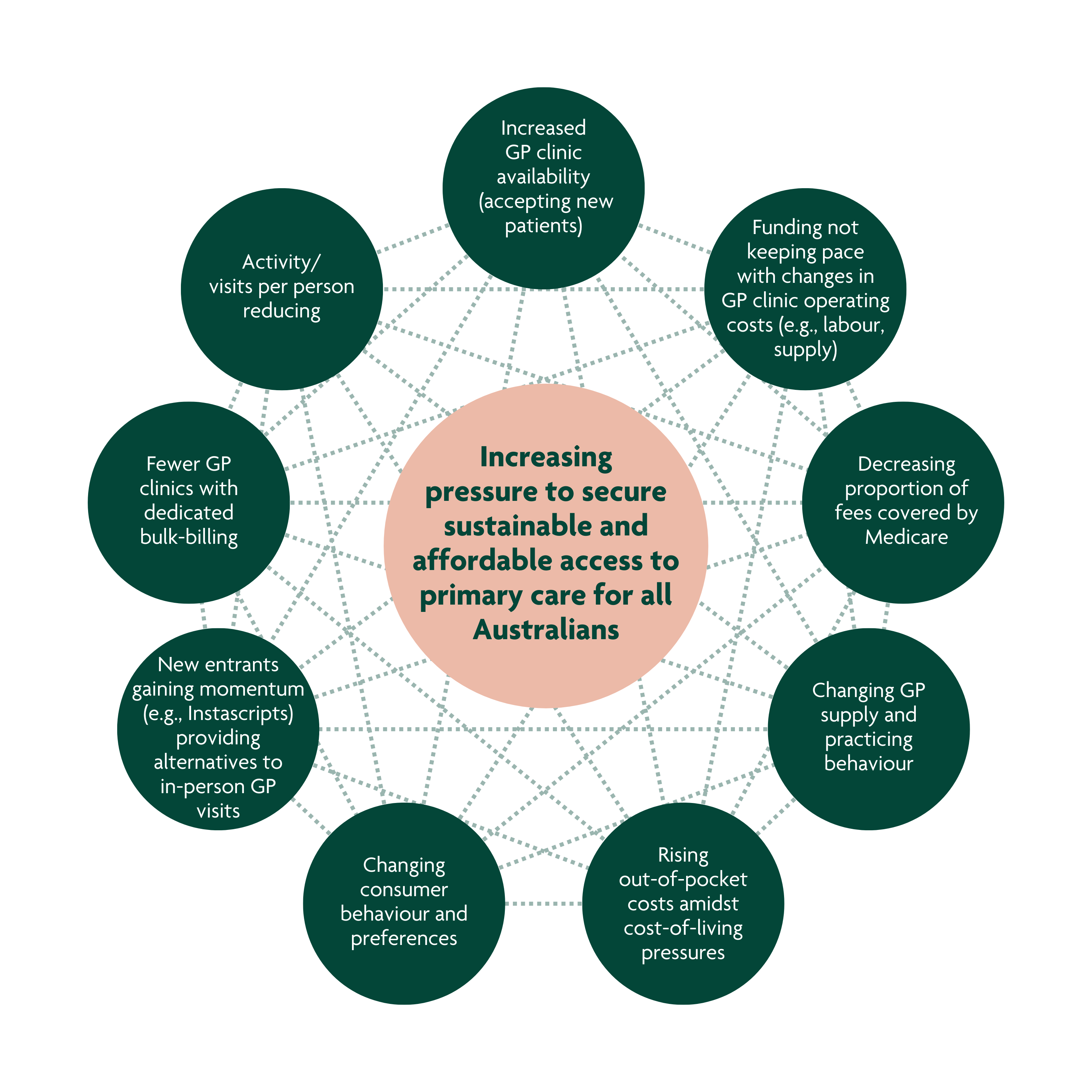

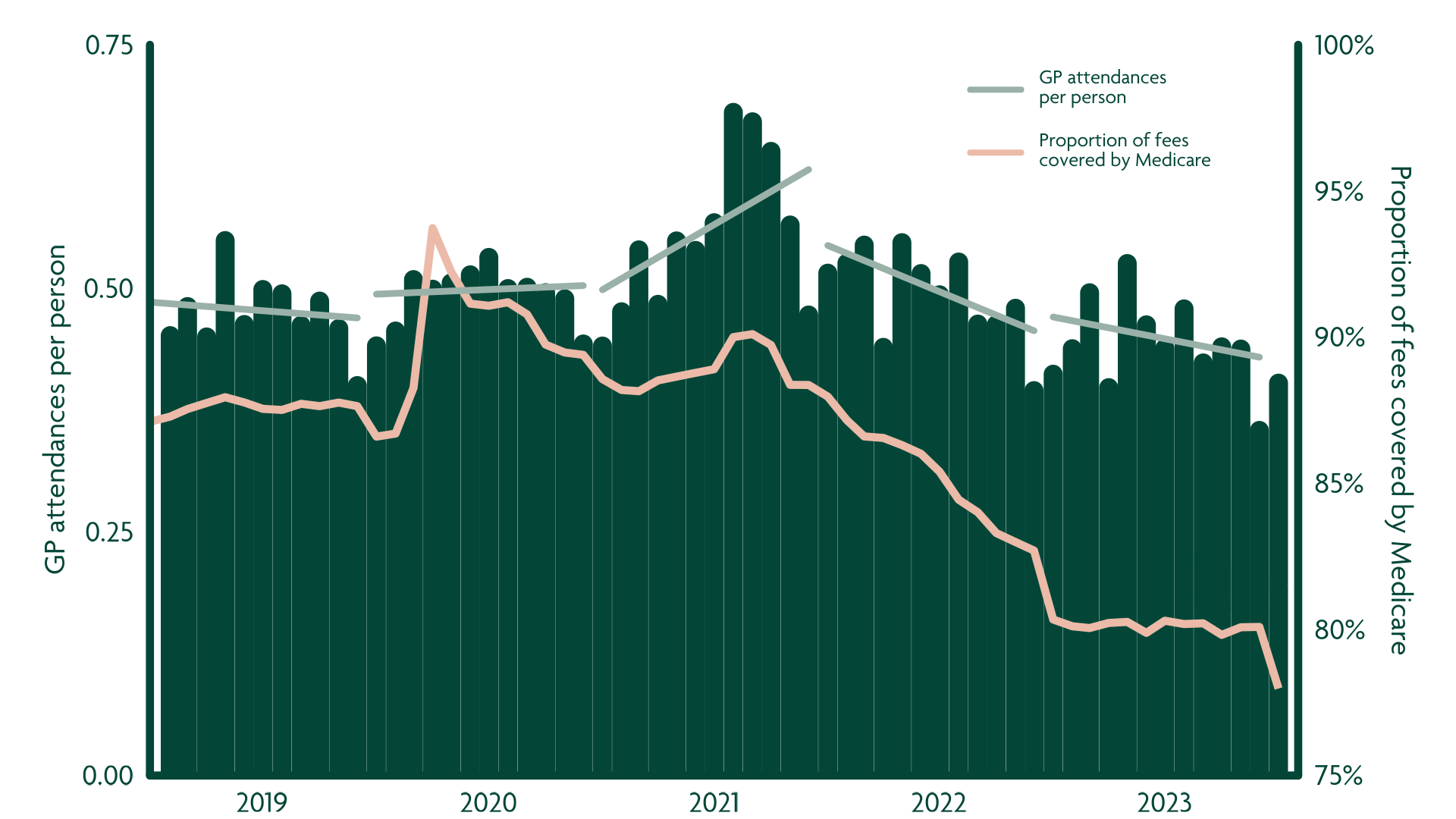

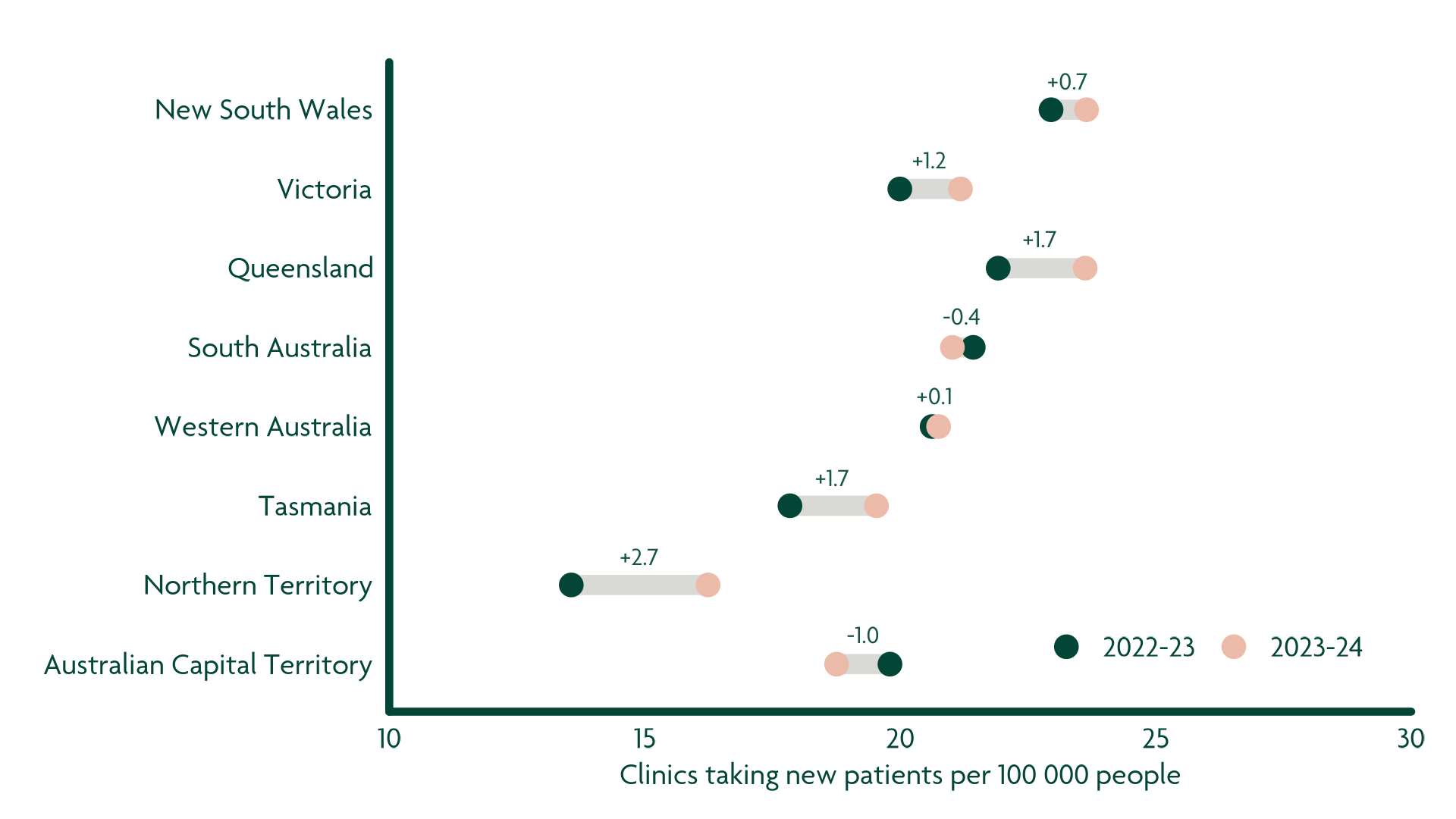

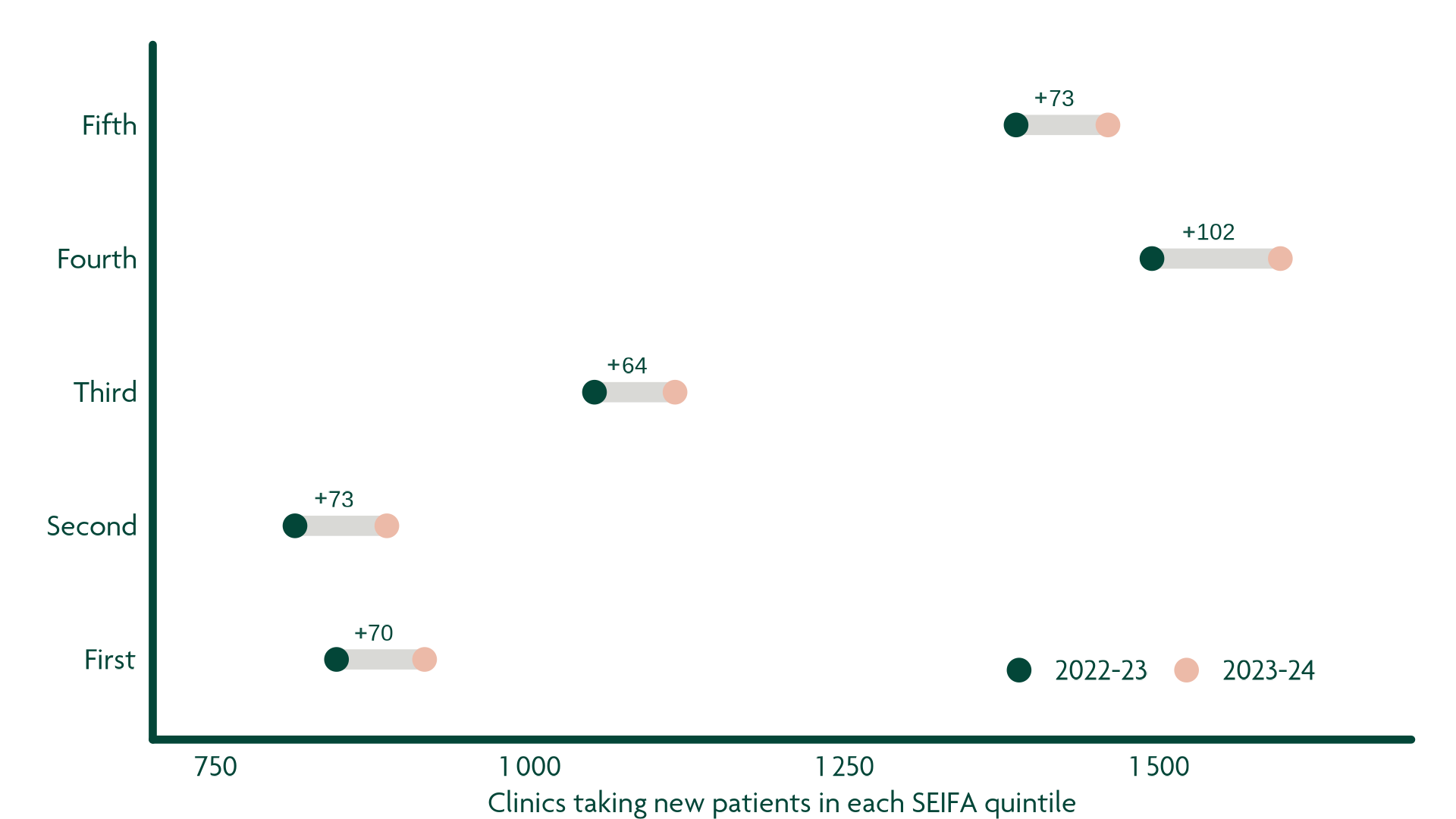

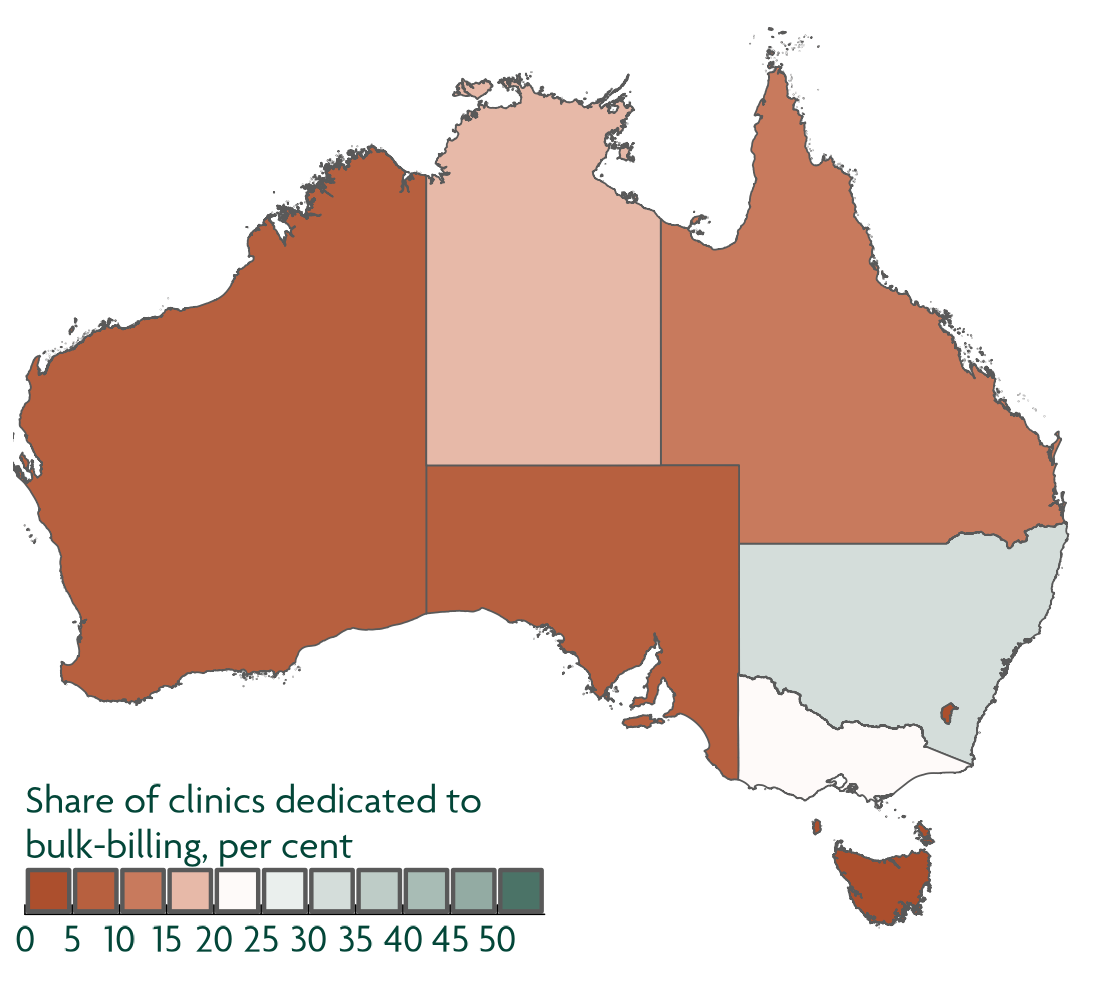

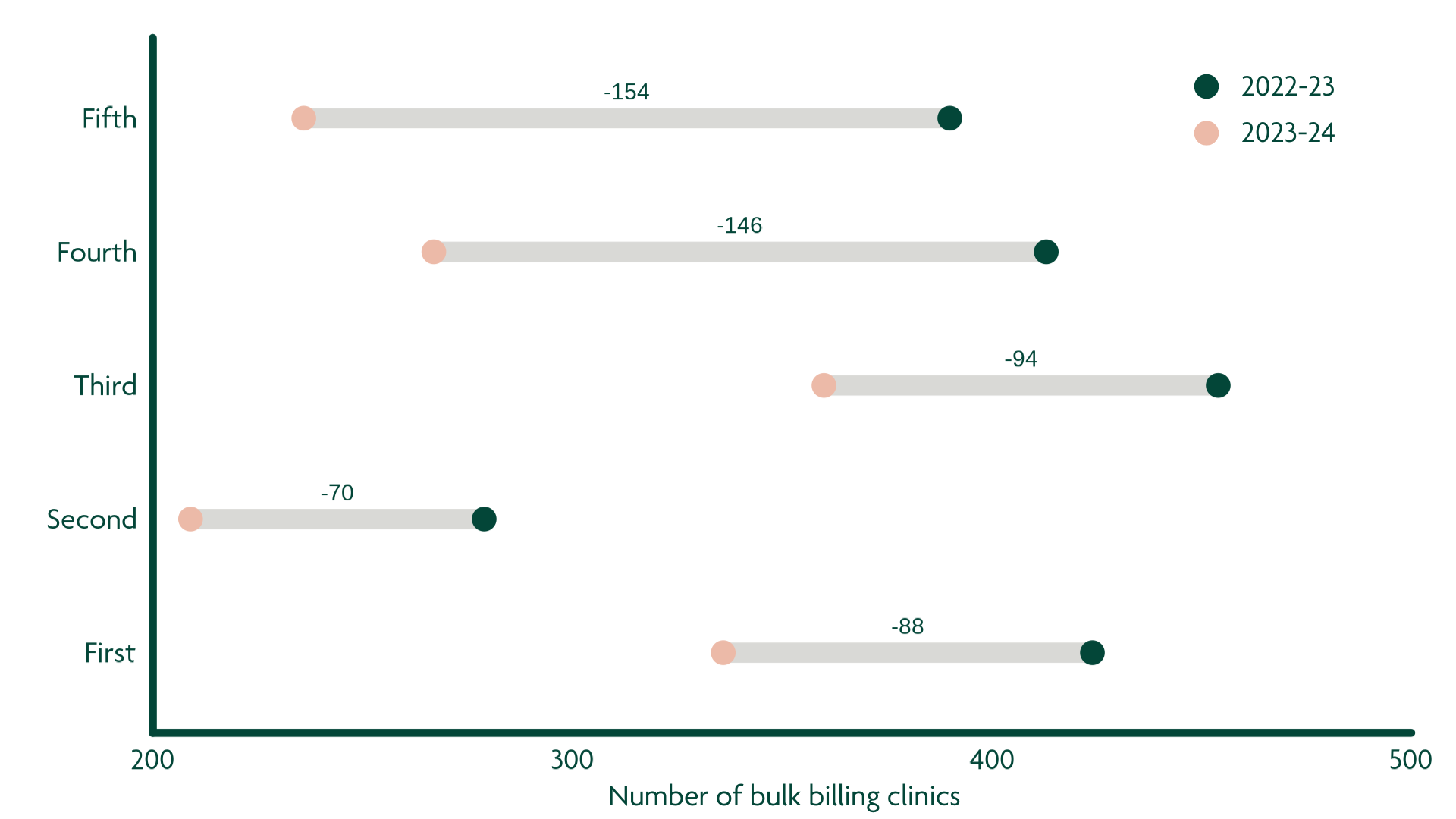

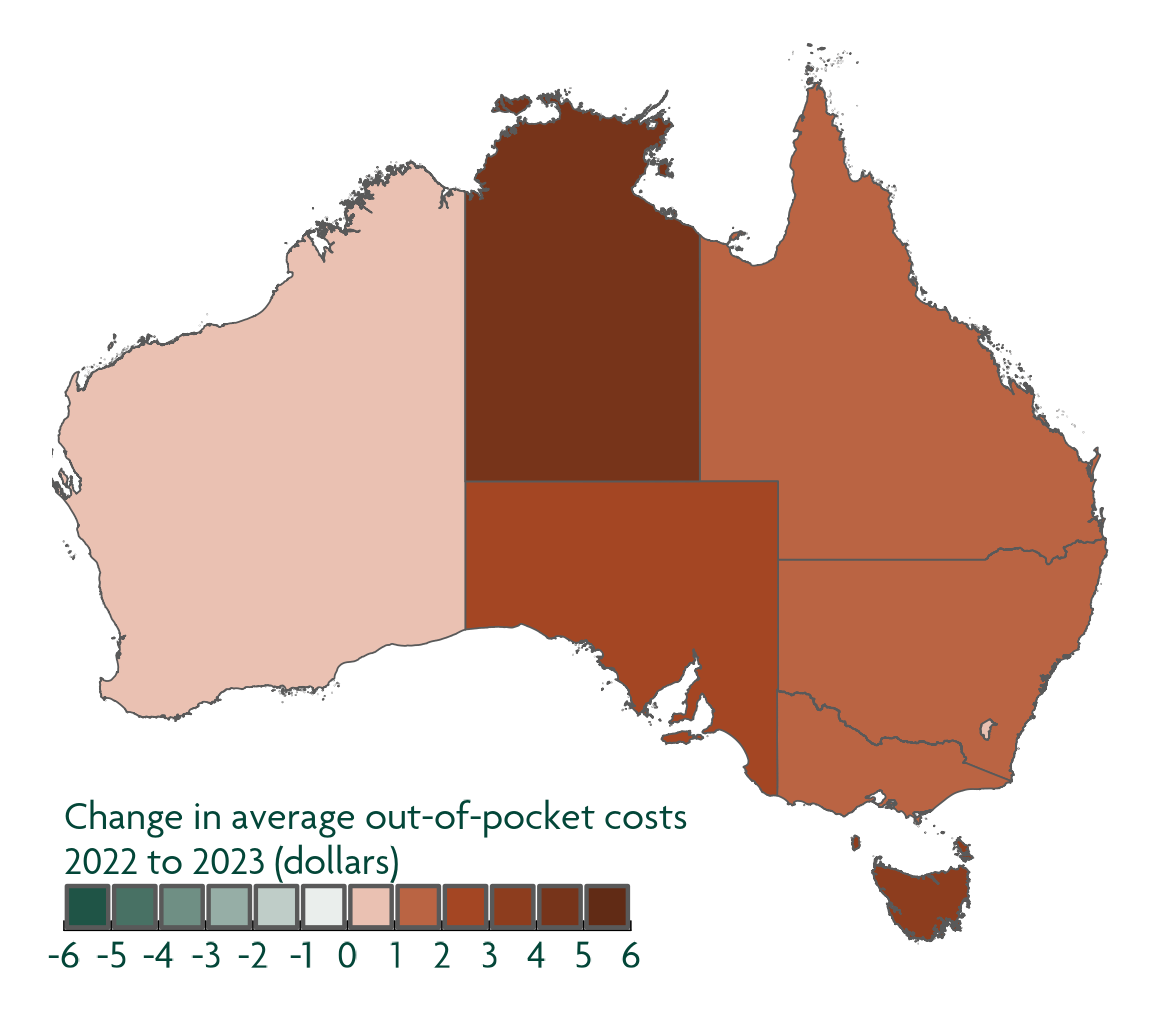

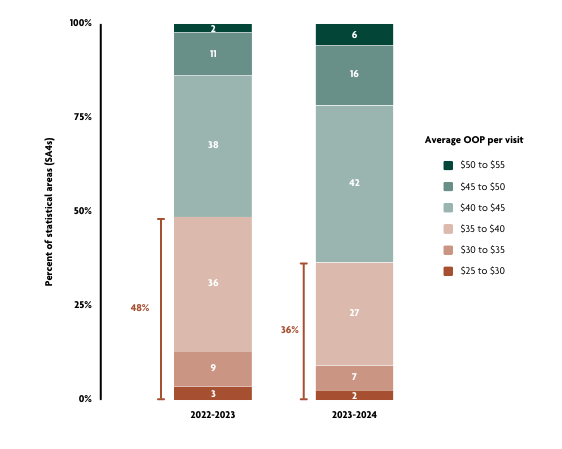

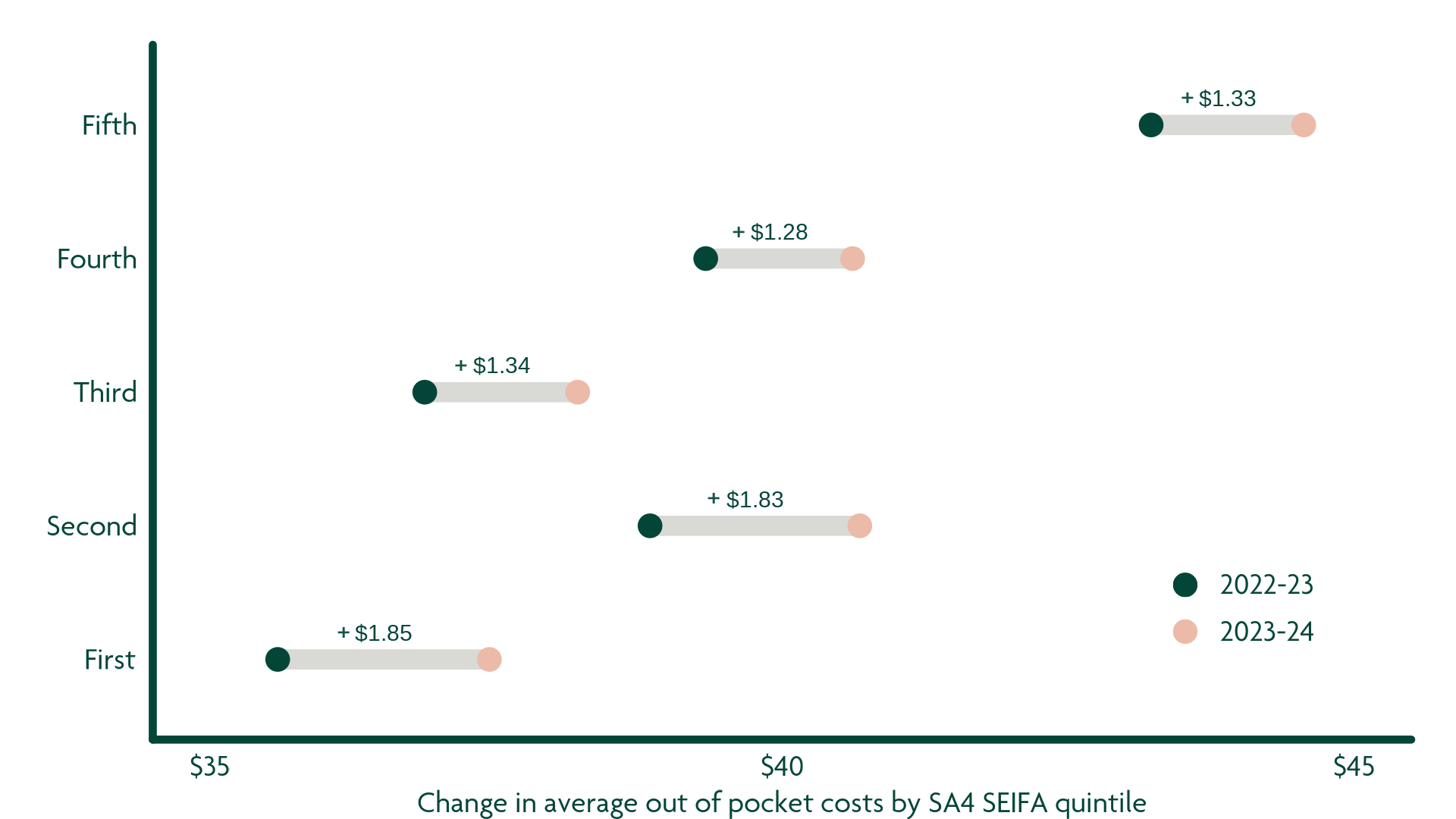

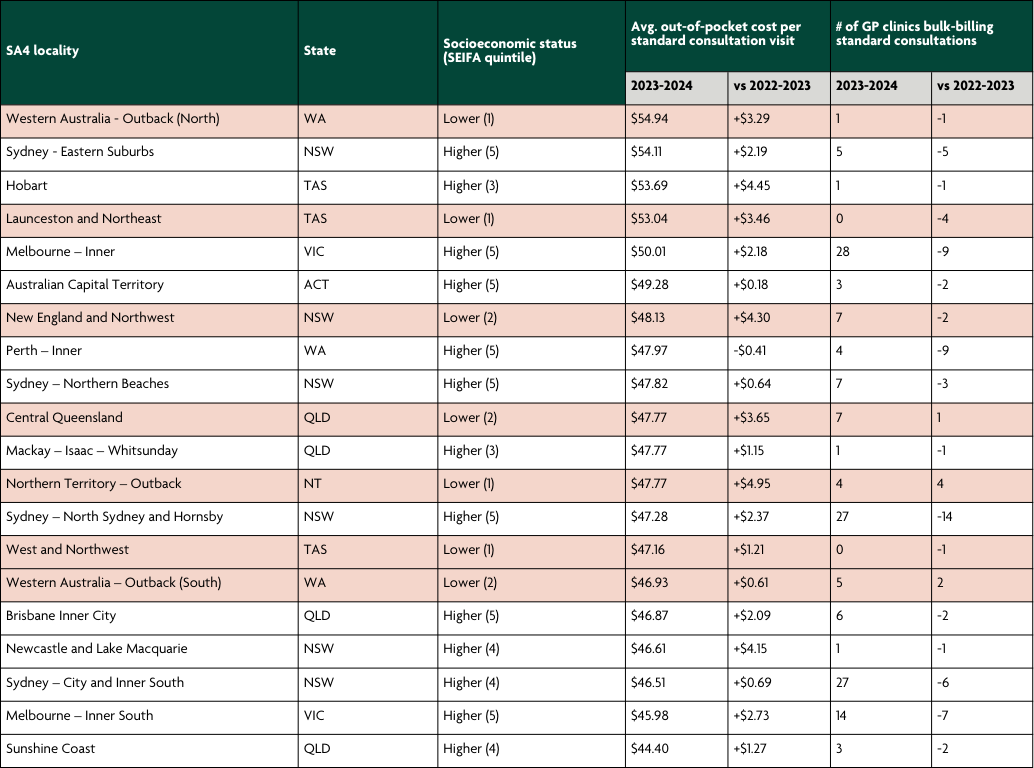

Amidst growing cost-of-living pressures, the number of GP clinics bulk billing standard non-concession adult consultations has decreased. In this article, we unpack some of the factors likely contributing to the decrease and explore some of the potential access implications. We hope this will spark curiosity and encourage a conversation about how to ensure that access to primary care remains affordable into the future for all Australians.